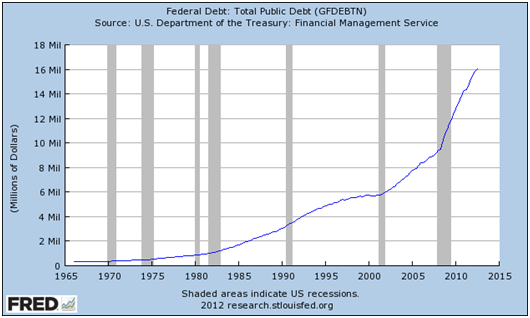

Wrangling over the debt ceiling in the U.S. took center stage for weeks and we look at the whole episode as a sad sign of the times. It will likely become ever more commonplace. Governments across the globe are fighting to continue deficit spending and politics has forced central banks to take huge gambles by buying up enormous sums of debt. It is a global Ponzi scheme and a game of currency debasement. Those who recognize the recklessness of these policies push back and are castigated by the many in the media and various pundits as if being upset about handing the next generation a horrific set of fiscal circumstances makes one a pariah or worse.

Our best guess is that those who favor these policies should expect more frequent pushback as it becomes obvious to most that they are not working and have unintended consequences. Common sense dictates that various vested interests will continue to argue over priorities because real money (as opposed to the printed variety) is scarce. Many will continue to argue that putting our heads in the sand is just fine and that our debt binge is not an issue. Nonetheless, government involvement in markets and the economy is just about all there is these days. Five years into a supposed recovery the Fed seems too fearful to even slightly diminish its QE program. Before QE began even one $85 billion asset purchase program would have been a huge deal, but now a monthly purchase of that sum is the norm!

It seems as though everything that the powers-that-be do is a contrived effort to keep stock markets from collapsing. We think the Fed pays lip service to employment and inflation, but determines its success by where the S&P 500 closes on a given day. We do not say that lightly! Someone needs to tell them that QE is simply creating more free reserves because banks are not lending. We point to recent dismal reports from retailers, restaurants, and trucking companies as proof of policy ineffectiveness. At the same time, we know we have never could have imagined that so many stocks could trade at levels that reflect a robust business environment, yet the reality of their revenues and earnings paints a starkly different picture. This reality gap is a hallmark of monetary policy and one that must be resolved. Perhaps that will happen with a flat equity market for years without a major correction, but expecting that scenario would be betting against about a hundred years of market history.

We think we are caught in this paradigm that requires the Fed to buy up Treasury debt largely because it creates a ripple in the market pond that causes investors to keep doing foolish things like buy equities at some of the richest valuations in market history. We have no way of knowing how long this powerful belief in magic can continue. We know a lot of money has been lost in years past during prior Fed easing cycles because sooner or later fundamentals take over. Many are relying on one year’s worth of expected earnings to make investment decisions. That often does not end well, particularly when profit margins are dramatically above long-term averages and revenue growth is hard to come by. We really do believe that the Fed has lost all credibility and simply targets the S&P 500, but many know this now and believe they can exit before the party stops. We have no way of guaranteeing that with our capital and cannot take the risk.

Janet Yellen has gotten the nod to head the Fed, so don’t look for any changes in monetary policy. She may talk about shrinking the enormous $85 billion monthly purchase plan. She may even try it for a period of time….until stocks correct 10% or so. In fact, if it’s possible, we suspect that she will be even more accommodative given her public comments and demeanor. She, like Bernanke, really believes the Fed can create employment in the face of structural issues that are beyond her control. Many of the unemployed remain so because there are not enough of the types of jobs created by the Fed’s last bubble in housing. Given the cruel nature of markets, it is likely that money printing will continue until QE becomes the two most loathed letters on the planet in coming years. Based on history, it is the expected result given the tremendous accolades now being piled upon the academicians at the Fed. Greenspan was a celebrated legend before the tech bubble burst in 2001. Of course, Bernanke has been given recent credit for saving the world after the housing insanity which he helped create, but he was far from rock star status right after the 2008-09 crash.

The equity market is a market of individual stocks. In the end, the dynamic has become one in which faith in the magic of QE is pitted against the reality of individual company earnings reports. We strongly suspect that over the coming quarters too many companies will disappoint investors, causing their stocks to swoon and ultimately taking indices with them. We invest based on valuations, so we worry ourselves with what we can control. The Fed is either going to keep pumping dollars into the world or it is not. Investors are either going to persist in their belief that QE will magically boost stocks or they will become worried that QE is not helping the real economy as free reserves build and money velocity continues to crater. We do know that earnings have begun the process of rolling over and it is inordinately difficult to find equities to purchase.

We also know that QE punishes savers who would without a doubt have more disposable income if the Fed were not guiding all into riskier assets at rich prices. We suspect that Fed policy makes capital cheap for businesses and labor expensive, yet the FOMC wonders why employment is stagnant. We also know that it must be impossible for many businesses to conduct long-term planning because everyone knows that just about nothing in the current economic environment is organic or sustainable.

We are not paid to be optimists. We are paid to be realists.

The views expressed on this blog are the opinions of the authors. This information is not intended as investment advice or to recommend the purchase or sale of securities. More information on Strategic Balance, LLC may be obtained by contacting investor relations.

Does the FOMC deserve an “A”?

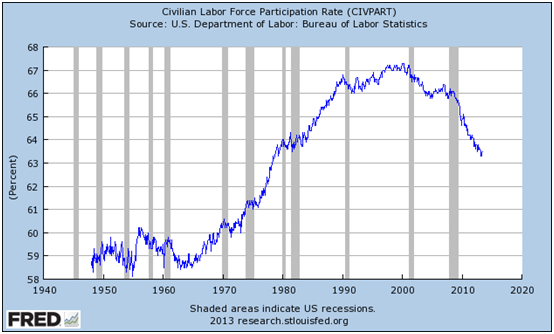

Listening to the leaders at the Fed these days is like hearing the best students in the class arguing with the teacher over a grade. Much of the media seems like parents arguing on their child’s behalf. For the guys at the Fed, who mostly know academia and nothing else, low grades would be crushing if they were not delusional. The class in this case is Real Economy 101 in which the Fed has helped guide the labor participation rate to thirty-year lows. Too many twenty-something’s reside in their parents’ basements for lack of a good job and older workers have given up looking for work in droves.

Nonetheless, our brave students at the Fed are just certain as can be that money velocity will rise sooner or later, as their printed money finally gets put to productive use in the real world. Doubters like us must prove the “counterfactual” (a popular word among the FOMC acolytes these days) that things would be worse without the heroes at the Fed who have rescued us every five years or so from the popping of the bubbles they helped blow.

The FOMC swears it deserves an “A+” because stock prices are so elevated and speculation is rampant again. Numerous pundits praise the wisdom of Chairman Bernanke. However, for the first time we can recall, a number of significant money managers and captains of industry have voiced concerns that a bubble has formed in many asset classes. But the Fed supposedly knows better! Though there is so little real world experience within its ranks, somehow the central bankers’ good grades in school and fancy research papers replete with indecipherable squiggly lines trumps the wisdom of people who really do not have a vested interest in sounding cautious.

We will give them their coveted A+ in one subject: Bubble Formation 101. They have been receiving that grade for over twenty years. Equity bulls are now running over 3.5 to 1 versus bears according to sentiment surveys. Margin debt and mutual funds flows are at euphoric extremes. Tech companies with no earnings are priced into the stratosphere. A++! We also give them an A+ in Capital Misallocation Strategies 101. The FOMC is causing money to flow into markets and not into productive capital. They openly sell the “sizzle” of their magic trick. However, does the Fed think that business decision makers are so naïve as to believe anything in the current environment is real or sustainable? Will higher stock prices lead to job growth?

Why you may ask are we so hard on the Fed. It is because their policies at these extremes help so few and penalize so many, especially savers. Even some from the inside the Fed are beginning to recognize the shortcomings and unintended consequences of current policies. In a recent piece in the Wall Street Journal Andrew Huszar, the man put in charge of the Fed’s mortgage purchase program wrote:

“I can only say: I’m sorry, America. As a former Federal Reserve official, I was responsible for executing the centerpiece program of the Fed’s first plunge into the bond-buying experiment known as quantitative easing. The central bank continues to spin QE as a tool for helping Main Street. But I’ve come to recognize the program for what it really is: the greatest backdoor Wall Street bailout of all time.”

Better late than never we suppose.

By the most important measures, U.S. stocks are the most richly valued that they have ever been in about 100 years of history, in spite of the underlying economy needing life support and pain killers for five years now. We predominantly use normalized earnings to value equities in an effort to adjust for cyclical earnings variability and typical profit margin behavior, but a more direct and less “geeky” way to get to largely the same answer is to compare stocks to annual revenue figures. On that front, data-centric fund manager John Hussman recently wrote:

“While the valuation of the S&P 500 Index itself was higher in 2000, it’s notable that the overvaluation of the S&P 500 was skewed in 2000 by extreme overvaluation in very large-capitalization stocks, while smaller capitalization stocks were much more reasonably valued. In contrast, we have never in history observed the median stock as overvalued as we observe presently. Indeed, the median price/revenue ratio of stocks in the S&P 500 now exceeds the 2000 peak. Likewise, as Damien Cleusix has observed, if we examine valuations by quartiles (25% of stocks in each bin), the average price/revenue ratio of the two middle quartiles also exceeds the 2000 extreme.”

Yet comically, former Chairman Greenspan had the audacity to recently argue stocks are cheap.

The next Fed Chair, Janet Yellen, just told us today during her confirmation hearing that there is no “over leveraging in the markets” and no “misalignment in asset prices.” Why worry?

The views expressed on this blog are the opinions of the authors. This information is not intended as investment advice or to recommend the purchase or sale of securities. More information on Strategic Balance, LLC may be obtained by contacting investor relations.