In a replay of the last few years, pundits, prognosticators, and Wall Street universally proclaimed that all was right with the world as a new year commenced. Congress allayed “fiscal cliff” concerns for the time being by postponing discussions of spending cuts in spite of the unsustainability of current deficits, igniting a big equity rally during the year’s first week. Earnings reports were not bad enough to stop the frenzy, especially as Japan began jawboning about its latest and greatest quantitative easing effort.

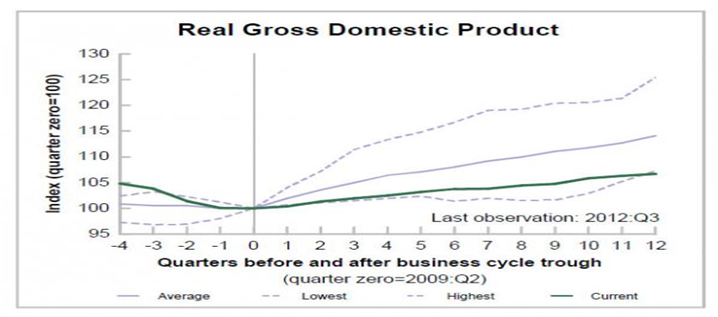

I am not sure the “talking heads” need much of anything to justify spouting positive views on all matters and ignore or minimalize anything even remotely negative. That disdain for facts and objective reality has been going on for a few years. The commentary (cheerleading) as the fourth quarter played out would have led one to believe we were in a real recovery, not one that even recent St. Louis Fed data depicted as the worst ever. Just look at their graph below to see why.

I admit it was entertaining to listen to the convoluted logic as the mainstream media explained how the just released real GDP number for the fourth quarter (not in above graph) which came in at -0.1% is a good thing….just like the multi-decade high level of long-term unemployment or the near 40% decline in Apple’s stock (we have been short that one). Real GDP would have been even lower had the U.S. Bureau of Economic Analysis (BEA) not monkeyed with the deflator. Of course, the Fed will just do more money printing, which is everyone’s favorite reason why one should buy anything and everything. Therein lies the bulls’ hopes, but additional QE will probably not provide much to change the current doldrums based on past results.

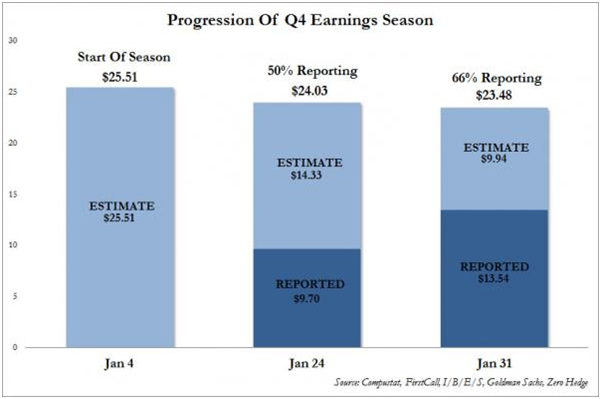

January was replete with fourth quarter earnings reports. Based on how markets reacted, we think we must be looking at different financial statements than the crowd. Revenue and profit growth is very hard to find among the plethora of companies that reported. Numerous cyclical companies are experiencing significant revenue declines and cloudy futures. Overall, the graph below depicts how fourth quarter earnings estimates have moved significantly lower as more companies report.

Nonetheless, stocks raced higher as investors could not seem to get enough. We remain true to our convictions which averted a lot of pain in 2008-09. Emotion is running high, but we strongly favor math, which is the only reliable compass over time.

The views expressed on this blog are the opinions of the authors. This information is not intended as investment advice or to recommend the purchase or sale of securities. More information on Strategic Balance, LLC may be obtained by contacting investor relations.

")

The Stuff You’re NOT Hearing

As the equity markets continue to hover in the stratosphere, we think it’s important to highlight some key facts and figures that we are not sure you will hear them anywhere else. Consumer confidence fell in January to a 14-month low and is probably a partial reflection of the payroll tax hikes that hit during the month, which will be difficult for stretched consumers to overcome. This tax increase amounts to about $2,000 annually for many and obviously even more for those in higher brackets. Prices at the gas pump have begun to get more painful again and are the highest for this time of year ever.

Obamacare taxes will be hitting too and marginal tax rates were just raised for many so that the spending circus in DC can continue. Unemployment just ticked up to 7.9% and we know that many small businesses will be looking to shrink below the 50-employee level to avoid entanglement in the morass we call healthcare reform. In general, transferring wealth from the private to public sector will continue until “we the people” say stop.

Many localities again lowered tax assessed values for residential real estate in 2012 in spite of the Wall Street proclamations that housing is strong. We do not argue the fact that major homebuilders have seen a big pickup in activity, but this bounce off of the bottom for them does not alleviate the pressure of so many underwater mortgages. Also, the mortgage underwriting is much more stringent today than it was a few years ago in the sense that there actually is one now, so gains in the sector will be slowed by that process.

Europe, particularly Spain and Italy at the moment, continues to represent an enormous risk due to credit issues in spite of the declarations that all is well overseas. Spanish unemployment has recently hit 26% and housing remains in a depressed state as their GDP contracts and bank loan losses mount. German retail sales fell 1.7% in December versus November in another sign the economy there is struggling. Most of the continent is in recession. EU unemployment rose to 11.7% in December. Bear in mind that the only reason bonds of the most troubled nations have rallied in the last six months is that the ECB has provided a backstop, but there has been no fundamental reform or credit improvement, just an enormous buildup of risk on central bank balance sheets.

To counter the global malaise, Japan has fired another round in the currency war as its government debt overwhelms its economy. We fear that recent Japanese efforts to devalue through QE may have taken the “beggar-thy-neighbor” mentality to a more dangerous threshold as many nations race to cheapen their currencies versus that of trading partners in order to attempt to meet future obligations with debased monetary units and boost exports. Japan has no choice because its debt-to-GDP stands at a frightening number of over 200%! The aging of its population has caused it to cross the Rubicon…not enough workers paying taxes to cover all of the government’s obligations. Our Congress and the Fed should pay close attention. After the Nikkei 225 equity index hit 39,000 in 1989 during an asset bubble it now stands near 11,000, despite numerous QE efforts and too much government spending for twenty years.

Whether one thinks the global economy is ready to boom or crater, so much good news is reflected in equity valuations that there is no room for error. It is difficult to find voices recommending caution towards markets even as indices flirt with new highs. We find this “throwing in the towel” to be irrational based on historical metrics, but we have witnessed similar lemming episodes in prior cycles. We know we can’t remember a time when it was so difficult to find cheap stocks to purchase. Even during the crazy days of the tech bubble in the late 1990’s it was possible to find quite inexpensively valued equities in the small cap and mid-cap sector.

The views expressed on this blog are the opinions of the authors. This information is not intended as investment advice or to recommend the purchase or sale of securities. More information on Strategic Balance, LLC may be obtained by contacting investor relations.